By Jennifer Heathcote, vice president, Business Development, GEW (EC) Limited

On March 6, 2024, the US Securities and Exchange Commission (SEC) voted 3–2 to adopt The Enhancement and Standardization of Climate-Related Disclosures for Investors. The rule requires all entities registered with the SEC to disclose climate-related information. It was proposed in March 2022 and was meant to be published in the Federal Register following a legally required public comment period. After receiving more than 24,000 comments, 4,500 letters and various litigation threats from those concerned with the rule’s impact on businesses and the economy, as well as the difficulty in directly connecting weather-related business risk to climate change, the SEC softened the rule and delayed adoption by two years. The final 886-page rule ultimately was published in the Federal Register on March 28, 2024. Compliance will be phased in between 2025 and 2033. The rule in its entirety can be downloaded from the SEC website. 1,2

On March 6, 2024, the same day the rule was adopted, lawsuits challenging the SEC’s authority to mandate regulations not previously approved by Congress were filed in the US courts by 25 states, companies and business groups arguing the SEC overreached. Others, such as the Sierra Club and Natural Resources Defense Council, insisted the SEC should have done more. On March 15, 2024, the 5th Circuit Court of Appeals granted an administrative stay on the rule and, on March 21, a US judicial panel consolidated at least nine of the lawsuits into a single case to be heard by the randomly selected St. Louis-based 8th Circuit Court of Appeals. Pending the court’s ruling, implementation and enforcement of the SEC’s Climate-Related Disclosures rule temporarily is paused. The 8th Circuit ultimately will decide the constitutionality of the rule and whether it can proceed. 3

The SEC is an independent agency of the US Federal government. According to its website, www.sec.gov, the SEC protects investors, promotes fairness in the securities markets, and shares information about companies and investment professionals to help investors make informed decisions and invest with confidence. The purpose of the SEC’s Climate-Related Disclosures rule is to provide transparency to investors regarding potential climate-related risks to publicly traded companies, strategies those companies are pursuing to mitigate climate-related risks and foreseeable losses due to extreme weather events. The Climate-Related Disclosures rule applies to medium and large, foreign and domestic, publicly traded companies listed on US exchanges and all companies pursuing an initial public offering (IPO). Any company not legally required to register with the SEC is under no obligation to comply with the rule. The SEC estimates that approximately 2,800 companies will be impacted by the rule should it proceed as written. 4

Readers are encouraged to consult other resources, professional advisors and the rule directly for a full understanding of what registrants are required to disclose in financial statements. An SEC fact sheet 5 summarized the disclosures as:

- climate-related risks and their actual or likely material impacts on the registrant’s business, strategy and outlook;

- registrant’s governance of climate-related risks and relevant risk management processes;

- registrant’s greenhouse gas (“GHG”) emissions, which, for accelerated and large accelerated filers and with respect to certain emissions, would be subject to assurance;

- certain climate-related financial statement metrics and related disclosures in a note to its audited financial statements; and

- information about climate-related targets and goals, and transition plan, if any.

One notable change the SEC made to the final rule was the elimination of Scope 3 greenhouse gas (GHG) emissions reporting. Reporting of Scope 1 and Scope 2 emissions remains intact but is waved for Smaller Reporting Companies (SRCs) and Emerging Growth Companies (EGCs). Scope 4 is not addressed.

The purpose of this article is to provide relevant context that led to the SEC rule and explain scope emissions. The article also draws a connection between increasing interest and use of UV curing – and more specifically UV LED curing – to set inks, coatings, adhesives and extrusions across a wide range of printing, coating and converting markets, and the need for companies to reduce scope emissions in manufacturing processes.

Greenhouse Gas (GHG) Emissions

Emissions refer to gases that are released directly into the air. Emissions originate from both natural sources as well as anthropogenic equipment and processes used in electricity generation, transportation, industrial facilities, commercial and residential buildings, agriculture, land use (including mining and energy drilling) and forestry. Some emissions have little to no impact on the environment, human health or climate. Others contain some combination of undesirable and potentially harmful greenhouse gases (GHGs), volatile organic compounds (VOCs), hazardous air pollutants (HAPs) and toxic air pollutants (TAPs).

While carbon dioxide gets the most attention, GHGs include multiple different gases in the lowest level of the atmosphere known as the troposphere (Figure 1). GHGs absorb outgoing infrared radiation from the earth’s surface and trap the radiated energy as heat in the troposphere.

Non-Governmental Organizations (NGOs)

Before digging into global climate-change policy, one first should understand non-governmental organizations (NGOs). The United Nations (UN) established NGOs in Chapter 10, Article 71 of its 1945 Charter. The premise was that the UN would approve citizen organizations for the purpose of providing consultative services directly to the UN. NGOs are meant to be independent and are designated by the UN with General, Special or Roster status. 6 They are neither a government entity nor a UN member state and operate under a mission statement that champions social, political or economic causes that align with overall UN objectives. While NGOs are not for profit, many function with annual budgets in the millions and even billions of dollars. They are funded through donations, grants, contracts, the United Nations, member nations and fundraising.

In its inaugural year, the UN granted 41 NGOs with consultative status. On December 31, 2022, there were 6,343 officially sanctioned NGOs. The full list can be downloaded from the UN website. 7 Many NGOs participate fully and directly in UN policy creation and decision-making. Over the years, the term NGO has been expanded to mean any non-profit organization. GlobalGiving Atlas (www.globalgiving.org/atlas/) provides a comprehensive listing of over 9.6 million non-profits, charities and NGOs. Only NGOs that apply and are granted status by the UN are able to participate in UN policy making.

Role of the United Nations in Driving Climate-Change Regulatory Policy

Beginning in the late 1970s and continuing to the present day, the UN through its conferences, commissions, policy papers, international treaties, global projects and affiliated NGOs made sustainability a legislative priority for member nations. Gradually, the UN became the foremost global policy maker regarding sustainability and sustainable development and the driver of global mandates meant to address climate change. In doing so, the UN positioned itself as the arbiter on what is and is not sustainable and which anthropogenic activities are deemed favorable or detrimental to the world’s climate.

Through policy making, global projects and a growing administrative stage, the UN and activist NGOs have a direct impact on how individuals, businesses and governments throughout the world operate on a day-to-day basis with rules and mandates specifically enacted for the purpose of achieving sustainability and climate change targets championed by the UN.

What Led to the SEC Climate-Related Disclosures Rule?

In December of 1997, a UN hosted event oversaw the adoption of the Kyoto Protocol, which requires countries to reduce emissions of six greenhouse gases in an effort to slow climate change. The Kyoto Protocol is an international treaty signed by 192 countries. It was developed between 1993 and 1997 with the participation of 187 NGOs.

In 1997, two NGOs, the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), partnered to develop the Greenhouse Gas Protocol. It was published in 2004. The purpose of the protocol was to establish a standardized global method of GHG accounting. The 2004 protocol defined Scope 1 and Scope 2 emissions and provided guidance on how emissions should be measured and reported. In 2011, the protocol added Scope 3 and, in 2017, Scope 4 was introduced. Scope emissions are explained in the next section.

In the United States, per the US Constitution, international treaties have negligible domestic impact unless ratified by a two-third majority vote in the Senate. During recent decades, however, the precedent has been established where international treaties are legally recognized even without ratification if signed by the President. In lieu of a signed treaty, desirable aspects can be carved out and passed as local, state or congressional legislation. Congress also can grant rule-making authority to a subset agency of the government, such as the Environmental Protection Agency (EPA) or the Securities and Exchange Commission (SEC), among others. These agencies often will exert their own authority without congressional approval, as is the case with the SEC’s Climate-Related Disclosures Rule.

In 2005, UN Secretary-General Kofi Annan formed a 70-person group from 12 different countries to develop principles for responsible investment. Principles for Responsible Investment (PRI, www.unpri.org 8) subsequently was registered as an NGO and granted UN consultative status. PRI is supported by the UN but is not part of the UN’s organizational structure. In 2006, PRI published a policy document by the same name and launched its initiative at the New York Stock Exchange. 8

The PRI promotes six key investment principles, known as The Principles, and recommends actions for incorporating Environmental, Social, Governance (ESG) issues into investment practices and financial evaluations (Figure 2). PRI was the first UN-driven policy document to reference ESG. A company’s ESG score is calculated by independent, third-party analysts, with a maximum obtainable score of 100. ESG scores are used by institutional investors to evaluate and compare business entities and countries when making investment decisions.

Institutional investment companies are encouraged to become a signatory to the PRI as a way to publicly demonstrate commitment to responsible investment and place it at the heart of a global community seeking to build a more sustainable financial system. 9 Over 5,000 institutional investment companies are signatories, including Blackrock, State Street, Vanguard, Fidelity and JP Morgan Chase.

A 2019 Harvard Business Review article noted that one or the other of Blackrock, Vanguard or State Street is the largest shareholder in 88% of S&P 500 companies, and institutional investors overall own 80% of all stock in the S&P 500. 10 As a result, institutional investors through proxy voting and influence are integrating ESG principles into the strategies of publicly traded companies and have been doing so since they became signatories of the PRI.

As more institutional investors became signatories to the PRI, they began petitioning regulators for standards that would better enable them to abide by PRI guidelines. In response, the UK Parliament created Streamlined Energy and Carbon Reporting (SECR) in 2018, with additional guidance provided in 2019. 11 SECR requires Scope 1 and 2 reporting in annual reports for publicly traded as well as large private companies. Scope 3 is voluntary. The SECR impacts approximately 11,900 companies. In turn, the EU implemented the broader Corporate Sustainability Reporting Directive (CSRD) in 2021. 12 CSRD requires Scope 1, 2 and 3 reporting and impacts over 50,000 companies.

In the US, the Securities and Exchange Commission published a rule entitled Enhancement and Standardization of Climate-Related Disclosures for Investors to the Federal Register on March 28, 2024. The final rules reflect the Commission’s efforts to respond to investors’ demand for more consistent, comparable and reliable information about the financial effects of climate-related risks on a registrant’s operations and how it manages those risks while balancing concerns about mitigating the associated costs of the rules. 1 The SEC rule requires large, publicly traded companies to report Scope 1 and 2 emissions and is anticipated to impact 2,800 companies. The rule currently is being reviewed by the 8th Circuit Court and is paused until a ruling on its constitutionality is made.

Scope Emissions

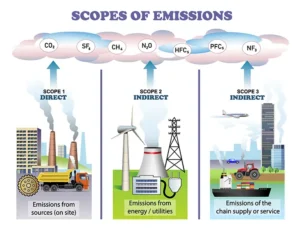

The NGOs World Resources Institute (WRI) and World Business Council for Sustainable Development (WBCSD) published the Greenhouse Gas Protocol in 2004. In doing so, they defined Scope 1 and 2 emissions. Scope 3 was added in 2011. Scope 4 was proposed in 2017. Scopes 1, 2 and 3 are illustrated in Figure 3. Scope 4 is illustrated in Figure 4. Additional information on WRI and WBCSD as well as the partner organization, GHG Protocol, and its services, global reporting standard and financial contributors is available at www.ghgprotocol.org.

Scope 1 emissions are direct GHG emissions resulting from equipment controlled or owned and operating on or within company assets as well as emissions from all transportation, construction, mining and off-highway vehicles directly owned and operated by the company.

Scope 2 is indirect GHG emissions resulting from the use of purchased electricity, steam, heating and cooling for a company’s own use.

Scope 3 is all other indirect GHG emissions from upstream and downstream supply chain activities not accounted for in Scope 2.

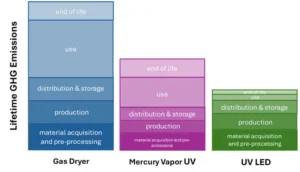

Scope 4 is emissions reductions that occur outside the value chain or life cycle of a product. Scope 4 supports development and adoption of products and services needed to achieve Net Zero. It often is referred to as mitigated, offset or avoided emissions (Figure 4).

Companies that manufacture goods which reduce reliance on fossil fuels and lifetime GHG emissions can positively promote their products through Scope 4 emissions. Potentially, this includes UV and UV LED curing systems with a theoretical example shown in Figure 4. The example compares lifetime greenhouse gas emissions for three different products used to set inks, coatings and adhesives in manufacturing processes. Scope 4 accounts for emissions incurred during material acquisition and pre-processing, production, distribution and storage, use and end of life.

The visual in Figure 4 is useful for comparing alternative products or solutions for the purpose of selecting the technology that best reduces emissions. In this hypothetical example, UV LED curing clearly has an advantage due to its all-electric, non-hydrocarbon operation; compact footprint; need for less installed transformer power; lower peak demand at start-up; reduced electricity consumption during operation; elimination of consumables, long life, and lack of GHG, VOC, HAP and TAP emissions during operation. Conventional UV curing also reduces lifetime GHG emissions; however, it consumes more electricity than UV LED curing and has ongoing consumables such as lamps and reflectors that must be regularly shipped to the facility, stored and properly disposed at end of life.

UV and UV LED Curing Lower Emissions in Industrial Processes

Manufacturers generally have three main categories they can target for emissions reductions. This includes electricity supply, transportation and industrial processes (Figure 5). Oil, coal and natural gas provide approximately 84% of all the world’s energy and roughly 64% of all electricity. 13 After 20 years and more than 5 trillion USD investment globally, hydrocarbon use has only decreased 2%. 14 As a result, solar and wind are not driving an energy transition. They simply are adding generating capacity to the grid, all of which must be fully backed-up by conventional power generation to prevent blackouts. Due to intermittent, weather-dependent generation and low energy density of solar and wind, insufficient supply of grid transformers, the massive and costly transmission infrastructure that must be built to connect remote solar and wind farms to the grid, and the massive quantities of batteries required, it is unlikely that large scale emissions reductions will come from solar and wind power generation alone. This is compounded by the rapidly increasing and potentially doubling electricity demand due to cloud computing services, artificial intelligence, manufacturing automation, electric vehicles and the overall push toward electricity powered everything.

In terms of transportation, 97% of all global transportation relies on oil. 14 With the exception of electric vehicles used for short travel distances, electric battery technology is unlikely to replace hydrocarbon-based fuels to any significant degree by 2050. Battery power simply is not viable, scalable, practical or affordable for most diesel-powered trains, trucks, earth moving equipment and cargo ships, as well as jet fuel powered airplanes. Oil-based fuels are the everyday workhorse energy source in most transport vehicles.

This leaves industrial processes. Since breakthrough technologies such as carbon capture storage (CCS) and green hydrogen are not yet technically, practically or economically viable and likely will not be operating at scale by 2050, manufactures should instead focus on existing technologies that already are proven, readily available, easily expanded and scalable now. One of those technologies is UV curing.

UV curing sources are all-electric and require no onsite burning of hydrocarbons. UV curing releases no GHGs, VOCs, HAPs or TAPs to the environment during operation. Since UV curing is a chemical reaction and utilizes 100% solid materials in inks, coatings and adhesives, there is no need for natural gas-powered ovens to evaporate water or solvent-based carriers. All that is needed is for the UV curing system to deliver the minimal threshold irradiance (W/cm2) in the spectral range required to react the molecules. Provided the delivered energy density (J/cm2) is suitable for the application line speed, curing occurs in a fraction of a second and in a relatively small footprint. As a result, UV curing allows for more efficient use of valuable production space. Because there are no long tunnel dryers and cure is instant, there also is less makeready, less scrap and less waste.

Formulations that are 100% solids reduce the weight of shipped raw materials since there is no added water or solvent-based carriers mixed with the resins, make clean-up easier and create little waste. This also means no water or solvent must be flashed away via forced hot-air or natural gas-powered ovens. No oxidizers or afterburners are needed to incinerate evaporated solvents before releasing them to the atmosphere. Workers also are not exposed to harmful solvent fumes, and there is no explosion risk. UV curing and the elimination of solvents make for a safer work environment.

Most notably, UV LED curing saves energy. Due to its lower power requirements, UV LED curing reduces total installed system power. This means a plant can run more equipment off existing transformers and pull less electricity from the grid. UV LED curing is instant ON/OFF and reduces peak demand at start-up. High peak demand is responsible for as much as 40% of a facility’s electricity bill. UV LED curing also consumes less electricity during operation. All of this together, means UV LED curing saves energy, saves money and reduces a manufacturer’s carbon footprint, even for facilities that already are net zero.

Because there are no GHG, VOC, HAP or TAP emissions, UV curing means zero Scope 1 emissions. Since UV LED curing reduces electrical needs and requires no on-site use of hydrocarbons, this benefits Scope 2 purchased power emissions. Manufacturers who use UV curing also have a positive impact on Scope 3 emissions in the supply chain due to reduced freight loads and material shipments, reduced scrap, reduced waste disposal and lower Scope 1 and 2 emissions. UV curing also makes the case for avoided emissions, which is Scope 4.

The recent legislative emissions mandates driven by the United Nations and implemented through the SECR, CSRD and SEC’s Climate-Related Disclosures rule are putting increased pressure on companies to reduce scope emissions. While these regulations currently apply to some medium and large private companies, as well as most publicly traded companies, the inclusion of Scope 3 emissions reporting in the European Union means that even small private companies in the supply chain may need to inform publicly traded companies of their scope emissions. Once scope emissions are regularly reported by an increasing number of companies, there will be greater pressure to reduce emissions annually. This is a significant reason there is growing use of UV curing and especially UV LED curing for a wide range of manufacturing processes. UV and UV LED curing reduce scope emissions, which ultimately benefits manufacturers, investors and society at large.

References

- US Securities and Exchange Commission. (2024, March 6). SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors. www.sec.gov/news/press-release/2024-31

- The Enhancement and Standardization of Climate-Related Disclosures for Investors AGENCY: Securities and Exchange Commission. 17 CFR 210, 229, 230, 232, 239, and 249. [Release Nos. 33-11275; 34-99678; File No. S7-10-22] RIN 3235-AM87. March 28, 2024. www.sec.gov/rules/2022/03/enhancement-and-standardization-climate-related-disclosures-investors

- Mindock, Clark. (2024, March 22). Challenges to SEC’s climate rules sent to conservative-leaning US appeals court. Reuters. www.reuters.com/legal/challenges-secs-climate-rules-sent-conservative-leaning-us-appeals-court-2024-03-21/#:~:text=March%2021%20(Reuters)%20%2D%20A,states%20and%20a%20business%20group

- Athrappully, Naveen. (April 6, 2024). SEC Forced to Halt Climate Reporting Mandate for Businesses. The Epoch Times. www.theepochtimes.com/business/sec-forced-to-halt-climate-reporting-mandate-for-businesses-5623236

- US Securities and Exchange Commission. (March 2024). FACT SHEET. The Enhancement and Standardization of Climate-Related Disclosures: Final Rules. www.sec.gov/news/press-release/2024-31

- United Nations Economic and Social Council. Introduction to ECOSOC Consultative Status. https://ecosoc.un.org/en/ngo/consultative-status

- United Nations. E/2023/INF/5. www.undocs.org/Home/Mobile?FinalSymbol=E%2F2023%2FINF%2F5&Language=E&DeviceType=Desktop&LangRequested=False

- PRI Association. (2006). An introduction to the Principles for Responsible Investment.

- Principles for Responsible Investing. Signatories Page. https://www.unpri.org/signatories

- Greenspon, Jacob. (February 22, 2019). How Big a Problem Is It That a Few Shareholders Own Stock in So Many Competing Companies? Harvard Business Review. https://hbr.org/2019/02/how-big-a-problem-is-it-that-a-few-shareholders-own-stock-in-so-many-competing-companies

- Guidance. Streamlined Energy and Carbon Reporting (SECR) for academy trusts. (Updated 14 February 2024). www.gov.uk/government/publications/academy-trust-financial-management-good-practice-guides/streamlined-energy-and-carbon-reporting

- European Commission. (2022). Corporate Sustainability Reporting Directive (CSRD). Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32022L2464

- Mills, Mark. How Much Energy Will the World Need? Praeger University Video. www.prageru.com/video/how-much-energy-will-the-world-need

- OurWorld in Data. Fossil Fuels. www.ourworldindata.org/fossil-fuels#:~:text=Globally%2C%20fossil%20fuels%20account%20for,summed%20together)%20across%20the%20world